The Indian Economy: Growth, Challenges, and Future Prospects

India has emerged as a global economic powerhouseover the last few decades, one of the world’s fastest-growing major economies. By 2025, Indian economy stands as the fifth largest economy in the world by nominal GDP and is the third largest by purchasing Shakti Samata (PPP). Its diverse economic structure, demographic advantage, and strong service and industrial areas have deployed it as a prominent player in the global economic scenario.

Historical references and economic reforms

After independence, India adopted a mixed economy model with significant government intervention and protectionist policies. This continued until 1991, when a serious balance of payment crisis forced the country to liberalise its economy. Economic reforms launched that year marked a significant turn, reduced business obstacles, encouraged foreign direct investment (FDI), and moved to a market-operated economy.

Since then, Indian economy has maintained a steady growth trajectory; in the last two decades, the GDP growth rate has been between 6% and 8% (preventing temporary global disruptions such as the 2008 financial crisis and the Covid-19 epidemic).

Major sector of the economy

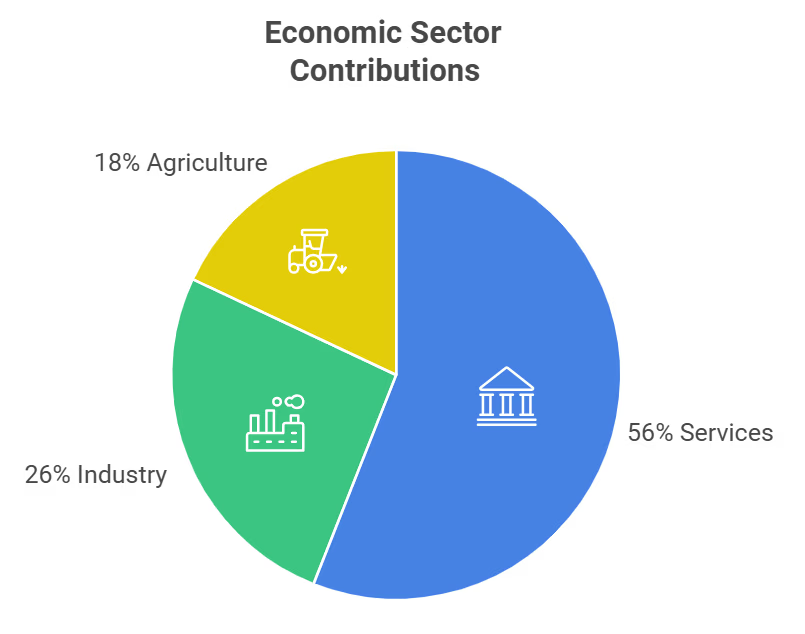

India’s economy is roughly divided into three major sectors: agriculture, industries, and services.

- Agriculture contributes about 15–18% of GDP, but approximately 45% appoints the workforce. Rural livelihood is still important; it suffers from issues such as low productivity, monsoon dependence, and inadequate infrastructure.

- Industry, including manufacturing, construction, and mining, contributes about 25–28% of GDP. The government’s “Make in India” initiative launched in 2014 is aimed at promoting domestic manufacturing and reducing dependence on imports.

- Services remain the largest and fastest-growing sectors, contributing more than 50% of GDP, remain the largest and fastest-growing sectors. IT and software services, telecommunications, finance, and e-commerce are important development drivers. India is a global leader in IT outsourcing and business process management (BPM), in which companies like TCS, Infosys, and Wipro are gaining international prominence.

Read also – https://bhanukakkar.store/battles-of-panipat-the-land-of-great-battles/

Demographic dividend and urbanisation

India’s population, which recently left behind China to become the world’s largest, provides both opportunities and challenges. More than 65% of Indians are under 35 years of age, causing the country to be rich in human capital. If properly trained and employed, this youth workforce can promote economic development for decades.

Urbanisation is also changing Indian economy geography. With more people moving to cities, infrastructure development, smart city projects, and investment in real estate are being seen. However, it also increases issues related to rapid urbanisation, housing, transport, and public services.

Major Challenges Facing the Indian Economy

For all of its supposed steep incline towards growth, Indian economy already faces several structural challenges:

- Unemployment: No jobs are really being created with the demand of the growing working-age population, especially in rural and informal sectors.

- Income Inequality: The gains from economic growth have not trickled down to all, resulting sometimes in even faster growth in incomes of some at the expense of others.

- Infrastructure Deficits: Power supply, transport network, and logistics still do not measure up to global standards.

- Bureaucratic Hurdles: Red tape and inconsistencies in policy-making can work against investment and innovation.

- Environmental Sustainability: With increasing intensive industrial activity and urbanisation, pollution, deforestation, and water scarcity have become issues of concern.

Outlook and Future Prospects

With digital transformation, manufacturing, and green energy transitions as its showrunners, Indian economy stands poised to become a $5-trillion economy in the coming years. Through programs such as Digital India, Startup India, and Production Linked Incentives (PLI), the Indian government seeks to improve productivity, innovation, and entrepreneurship in the country.

India is also investing in renewable energy, which aims to meet 50% of its energy requirements from non-fossil fuel sources by 2030. Meanwhile, its fintech and digital payment ecosystems are bringing revolution to financial services.

conclusion

The Indian economy is at a significant turn. With a combination of policy reforms, technological progress, and inclusive development strategies, India has the ability to not only maintain a high growth rate but also to take millions out of poverty and claim a strong role in the global economy.

Post Comment